23 May 2018

Three years ago, I wrote a post about preparing financially for a baby (my most-requested Marvelous Money topic at the time!). I promised in that post to revisit the topic at some point in the future when I actually had children, and I’m so happy to do so today! My angle: what it actually cost us to add a baby to our family in the first year.

Several of you have shared that you think of me as a “big sister” going a few steps ahead of you, which is wonderfully sweet and a title I take seriously. I want to share these numbers not because you’ll be able to copy and paste them into your own life, but because if you’re thinking about having children and wondering how it will affect your finances (hand of my younger self raised high!), it is incredibly hard to find useful numbers.

I hope this post offers some hope, helpful perspective, and fodder for conversation with your spouse! :)

First, a few details about the parameters I chose:

— Our daughter was born in January, which is excellent for sharing numbers, since we budget every dollar on an annual basis. I’ve included all of the June-related costs from 2016 here (unless otherwise noted), as well as the June-related costs from 2015 that we incurred while preparing for her arrival.

— I have not included the retail price of gifts we received, items we borrowed, etc. here — just what we actually paid out of pocket. Obviously, there is a HUGE range of prices for everything baby-related, and it can make a big difference how much you buy used or buy at all. This is not meant to be a universal cost breakdown but just a glimpse at one family’s expenses based on our unique circumstances and priorities.

— I did not include any healthcare costs, as those were paid for by savings in our HSA and I don’t consider them “out of pocket.”

— I did not include “shelter” costs (i.e. our mortgage) or transportation, since we would have had those anyway. I also did not include any portion of our grocery budget, because it did not change in June’s first year with us.

That should cover the preliminaries! Here’s the breakdown, with explanation following…

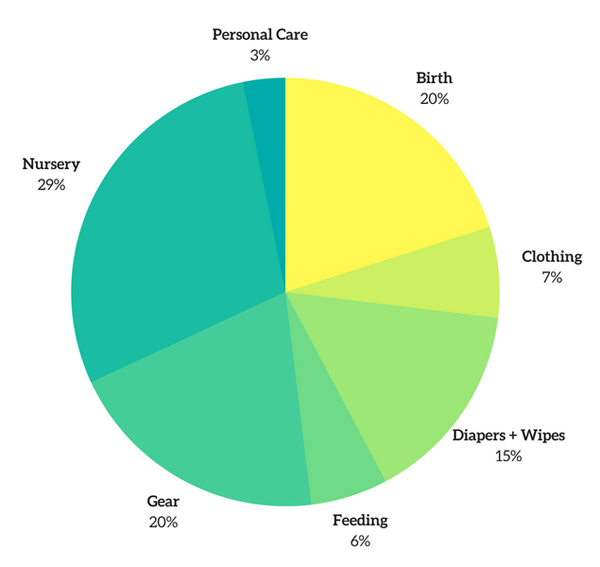

Birth: This included our birth class and our doula.

Books: I bought four pregnancy and parenting books – my favorites are here!

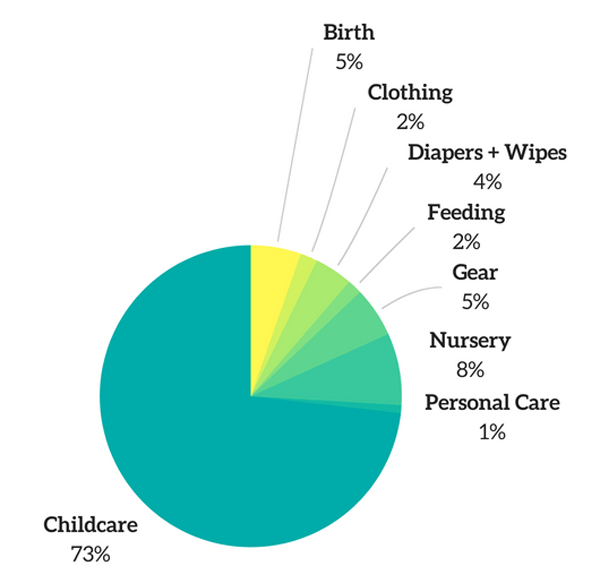

Childcare: This is by far the largest portion of the total, but I have not even an iota of regret about spending this money! There is almost nothing I would rather spend on than making sure June is safe, loved, and well cared for when we’re not with her, and we were so happy with the school we sent her to for her first year. This covered about eight months of care post-leave.

Clothing: We were incredibly lucky to receive LOTS of hand-me-downs from Nancy and my sister. The majority of the rest of June’s clothing was purchased at my favorite twice-a-year consignment sale, with a few additional special items here and there. I think this is a category where we saved a lot of money, especially considering we had a girl – ha!

Diapers and wipes: We almost exclusively used Water Wipes and Up&Up diapers and were very happy with both.

Feeding: This included our Kiinde supplies and some formula. Thankfully, breastfeeding dropped this category wayyy down!

Gear: This category included everything that we didn’t borrow or receive as a gift, including our baby monitor, our bassinet, a console for our stroller, a convertible car seat, baby gates, and more. You can read about some of our favorite gear at different ages in these posts!

Nursery: This was the only category whose total surprised me a bit, but we did have several large expenses that added up! The good news is that these purchases were the LEAST important, so they could easily be forgone if you’re on a tight budget. Larger purchases included the light fixture ($120); the glider, fabric, and upholstery ($475); a quilt for the twin bed ($110); and the Liberty fabric for the crib skirt ($154 – that stuff ain’t cheap!).

Personal care: This category included diaper cream, Nose Frida supplies, burp cloths, a thermometer, body wash, toothbrushes, and other toiletry type things!

Toys, gifts, and fun: Thankfully, babies don’t need too much to have fun :) This category included her beloved action stackers, a few books (we received SO many as gifts!), cups and a ring stacker, and the ukulele we got her for her first Christmas.

If you’re a visual person, here’s the breakdown in pie chart form:

And one with the major categories besides childcare:

There you have it! If you’d like to share, I’d love to hear how our breakdown stacks up to your own spending, or where you were able to save if you also have a sweet baby! Thank you, as always, for being so kind and thoughtful, friends!

Affiliate links are used in this post!

24 April 2018

As I wrote the How We Do It series, there were many topics – big and small – that I knew I would want to revisit at some point in posts of their own. When I got a few questions about how we jointly manage our finances in this post, I knew it was a great one to start with!

Using this beautiful image from Cultivate What Matters of the new Finance Goal Guide, launching today! If you have money goals you’re working toward, I think you’ll love this product!!

Many of the questions centered around why John and I have separate checking accounts. The short answer is that there’s no good reason – ha! Here’s the longer answer:

John and I have separate checking and savings accounts because we opened them before we were married, and there didn’t seem to be any good reason to open a new joint one after saying “I do.” After all, our accounts are at the same bank (and linked, so that we can access each other’s through our own dashboards!), and we of course have each other’s passwords. All accounts opened since our wedding day have been joint ones.

I know many people have strong opinions on joint versus separate accounts. I think many of the opinions, though, stop short of what’s truly important: the state of your heads and hearts trumps the practicalities of how your accounts are set up any day. All of the joint accounts in the world can still lead you to a dead end if you’re not pulling in the same direction.

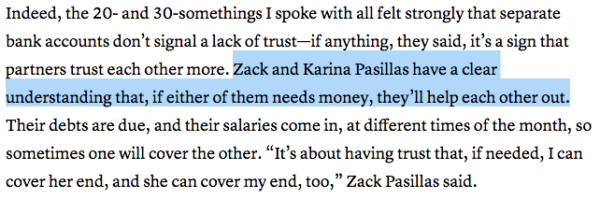

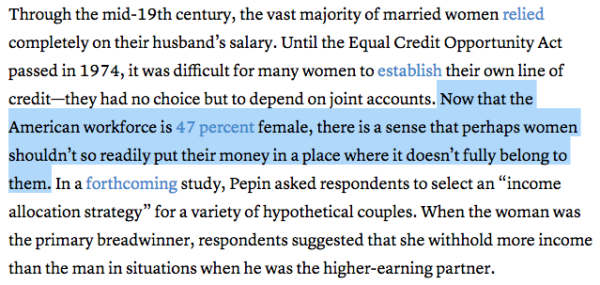

There is no “his money” and “her money” in our marriage. We have never valued each other or set individual spending levels based on what either of us make at our jobs. The idea of spouses effectively living at different income levels within a marriage is shocking and sad to me, as described in this recent Atlantic article:

They’ll help each other out?? Marriage means joining your financial future just as surely as it means joining your lives. I supported both of us while John searched for a job, and he put money toward my student loans for years without a peep of complaint. Were one of us to lose our job, we would not receive a “handout” from the other person – we would both adjust and bear the burden together.

On a practical note, the main reason there is no “his” or “her” money is that ALL money is fed into our family budget. At that point, we simply have one lump sum of money that we need to decide what to do with, together – it literally no longer matters who brought in how much. Because we’ve set the budget together, if it says we have a certain amount to spend, then that’s how much we have to spend. A budget is a great equalizer in this way, and if you need yet another reason to get on the budget bandwagon, there you go! :)

But back to the Atlantic article:

To that I would say, I don’t believe the money I bring home does or should “fully belong to me” — it’s shared with my husband, just as his money is shared with me.

Unsurprisingly, the arguments in the Atlantic article for why a couple wouldn’t merge their finances aren’t that compelling to me. There is one argument that I think does have validity, at least at the outset, but I don’t think it’s a situation that’s tenable longterm for a healthy marriage. If the two of you don’t have aligned beliefs on money, and aren’t consulting each other on where you’re hoping to go in life, then merging your finances absolutely will be a mess and will lead to arguments. The solution, though, is not to keep things separate — it’s to do the work to get on the same page.

John and I have a bit of an advantage here because we formed our thoughts on money alongside each other, but we also work actively to make sure we stay on the same page. (Hence our regular conversations and bimonthly net worth meetings!). Our friends Nancy and Will found themselves in the opposite situation: they came into marriage with VERY different ideas about how money should be managed. Financial Peace University helped them reach common ground, and they are some of the most inspiring financial stewards we know!

A final note, should you need more convincing: a joint budget not only determines your day to day spending on groceries, clothing, lawn care, and more, but it sets and guides your financial big picture, like how much you’re saving for retirement, how soon you’ll be able to get out of debt, when you’ll squirrel away the amount for a down payment goal, or how much you can give away each year.

And those big picture things? You want to work on them together, because then you will succeed together (and a lot more quickly than if you were working on your own!). There are few things more unifying in a marriage than reaching a major goal together, and if you’re not merging your finances, you’ll miss out on them.

Whew! Clearly this is a topic I’m passionate about, and that Atlantic article brought it all bubbling to the surface! To finish up, I’d love to hear: what goal are you working toward in your finances right now?

16 January 2018

Wow, y’all! I figured you would like this series, but I’ve been blown away by the response – I LOVED reading your thoughts on last week’s post on time, so thank you SO much for sharing! Truly.

To catch up any new gals: Nancy Ray and I are writing an eight-part series every Tuesday in January and February covering “how we do it” in eight different areas: the rhythms, habits, and routines that help us get things done and make the space and time for what matters most. You can read more of the backstory here.

Today’s topic is finances! I’m particularly excited about this post for many reasons (obviously), but one is that it really drives home what I love about this series: that you’re hearing from two people with similar hearts but different ways of living them out, showing that there’s no one right way to do things. Anyone who knows Nancy or I knows that we are both extremely passionate about financial literacy and freedom, but the fascinating thing is that “how we do our finances” is in some cases very different.

Let’s dig in! I wanted to begin with a few of the principles that guide John’s and my thinking on money, because all the tools in the world won’t be much help if your thought patterns are constantly conspiring against you. Here they are:

1. Whenever possible, we take advantage of the power of compounding and the time value of money. We want to make our money work for us as hard and as often as possible, which means starting NOW, even if that means starting small. Time is so powerful, and it’s the only part of the wealth equation you can’t make up. More about this here.

2. We remember we can’t judge anyone else’s financial situation from the outside. We might see a coworker going on a European vacation and be tempted to think we should be able to do that, but not realize they carry credit card debt or rent a super-small apartment or never eat out or don’t save for retirement. We try not to make decisions based on comparisons, especially since they’re always incomplete.

3. We believe our money has been entrusted to us. By God, to be clear :) And because we believe that, we feel an extra measure of responsibility to spend, save, and shepherd that money wisely and for the greatest good.

4. We believe money is a tool. It’s not inherently good or evil. I’d liken it to a chainsaw. It is very powerful, and very effective at what it does, but it can’t hammer a nail. You can’t expect money to do things it was never meant to do, like make you happy.

So how do these principles play out on a daily, weekly, monthly, and yearly basis? For us, it all comes back to the budget. We live and die by our budget, because without it, I’m sure we would be in very sorry financial shape. We make an annual budget and track it in a Google Doc. (Note: our doc and how we use it have changed a bit since I wrote that post five years ago, but it’s still a good overview!) It’s a system that requires some upkeep, but we’ve found a few things that make it easier: we commit to updating it twice a month (generally on the 1st and 15th, the same day we pay our credit card bills), and we almost exclusively use cards, so transactions are easy to reference and record.

That’s right, we use credit cards! I wouldn’t recommend them for everyone, but we pay ours off in full twice a month and have never carried a balance. The rewards (2% cash back for us) and the ease of tracking our spending make them the right fit for us. We have three: one predominantly used by John for his expense categories, one predominantly used by me for my expense categories, and one used by both of us for joint expenses (which include most things, including gas, groceries, gifts, dining out, June expenses, vacations, etc.).

We also each have a checking account and savings account (which we both have access to, but our paychecks get deposited into our respective accounts). I pay most of the bills out of mine, so to keep things simple, John simply “levels our accounts” on the 1st and 15th by transferring the difference from his checking to mine, so that we each have the same amount.

Our savings and checking accounts are at Capital One 360. I LOVE CAPITAL ONE 360! I’ve considered writing a Marvelous Money post just about this bank because I love it so much :) Why? The interface is great, there are no fees, and most importantly, they let you open as many savings accounts as you want!! Over the years, we have opened accounts to save for vacations, for our backyard renovation, for a new car, for our wedding, and many other things. You can give each account a unique name and set up automatic transfers each month, making setting aside a pool of money and building it over time fun and mostly painless! Highly, highly recommended. (NOTE that that is a referral link – I get $20 if you sign up, but I would NOT share something we didn’t adore! We’ve been customers since 2006 :))

Another thing that has simplified our finances: our charitable giving account. If you give away money regularly, whether to your church or other organizations, I would highly recommend one. I went into much more detail here, but the reason it helps simplify things is that at tax time, you only have to look one place to itemize your deductions.

I’m not going to chat too much about debt in this post because aside from our mortgage it’s not a huge focus for us right now, but if it is for you, I’d recommend checking out this post which talks about how we paid off my student loans!

Retirement savings are a priority for us, and we both have 401ks we contribute to through work as well as IRAs. Most importantly, we always make sure to contribute at least enough to get the full match our companies offer. Here is my beginner’s guide to 401ks and beginner’s guide to IRAs, if you’re new to this arena! We also use an HSA (Health Savings Account) as an important part of our retirement savings plan, as they are highly tax-advantaged. Might be something to consider if you have a high-deductible health plan!

A number of readers have asked me about 529s and college savings for kiddos recently, so I will likely write a separate Marvelous Money post on that topic in the future. We do have an account for June that we have contributed to, but I wanted to mention here that it is not a priority for us right now, given that we are going so aggressively after our mortgage goal. We feel confident with the overall plan we have, and know that we can make more progress without dividing our focus unnecessarily! Just like when you’re tackling debt, I think it is often most effective to pick one area of focus and go hard after that one instead of trying to implement five different things at once.

Finally, I wanted to briefly share how we divide up the financial responsibilities in our family. I think it’s equally important for each partner to have a role, AND for those roles to be clear and defined. These are ours:

Emily: Bill payment and account maintenance (activating cards, calling customer service, etc.)

John: Taxes, investment strategy, and “R&D,” or bringing new ideas to the table (like our tweaked mortgage plan)

Together: Set yearly budget, record transactions in the budget, and participate in our every-other-month “net worth” meetings

We call them that not because our net worth is so high (ha), but because they are when we look at a global picture of our finances and our budget. We look at what’s in each account, talk about changes to our budget or financial situation, progress we’ve made toward our goals, and more. To be clear, we talk about our finances on a more regular basis than every other month, but this is dedicated time we’ve set apart to cover more in-depth topics.

Friends, I hope this post was helpful for you!! Don’t forget to read Nancy’s post here. I’d love to hear what tool or practice has been most helpful for you in organizing your personal finances! Or, if this post brings up a question for a future Marvelous Money topic, I’d love to hear that, too! :)

The rest of the series:

Time: Em’s post and Nancy’s post

Finances: Em’s post and Nancy’s post

Home: Em’s post and Nancy’s post

Personal Lives: Em’s post and Nancy’s post

Work: Em’s post and Nancy’s post

Relationships: Em’s post and Nancy’s post

Kids: Em’s post and Nancy’s post

26 October 2017

One of my pet peeves about personal finance is when experts make blanket suggestions on how to save money. I think the way you spend (and save!) should be based on what you value. If you do this, you’ll not only find it easier to stick to your budget, but you’ll get greater pleasure out of the money you DO spend.

Though I dislike one-size-fits-all suggestions, I love being inspired by how others are finding ways to save. I asked six of my savviest friends for their favorite ways they shave their budgets, and added in a few myself — I hope they get your wheels turning!

Saving money on food:

I don’t eat meat during the week. I have a pretty consistent rotation of small and inexpensive meals that I eat for weekday lunches and dinners. Not only does it save me money, but I don’t get decision fatigue over deciding “what’s for dinner?” — Jess Metcalf, Content Manager and newly-engaged gal

We shop almost exclusively at Aldi, which cuts our grocery bill almost in half (compared to name-brand grocery stores). I make a dinner plan based on their weekly specials, which helps us eat in for the majority of the week with plenty of leftovers for lunches. — Samantha Ray, hair and makeup artist and blogger

Food spending has been a challenge for us (to put it lightly) but we’ve made significant progress by switching to getting vegetables from a CSA box and buying meat from Costco (organic meat at normal prices). We get the box twice a month and plan our meals based on what vegetables we receive. This has challenged us to think outside our recipe box/cookbooks and has significantly cut down on the number of ingredients we buy per recipe. — Dave Kirk, finance guy and husband

I can’t even imagine how much we’ve saved over the years by almost never buying alcohol. We don’t hate drinking, but it’s just not something that’s important to us, and therefore doesn’t make sense for us to spend money on! – Em

I use cash and a calculator at the grocery store! It’s our foolproof way to not blow the grocery budget. — Valerie Keinsley, stay at home mama and online stationery shop owner

Saving money on entertainment:

I solely order water at restaurants, unless I’m celebrating something, in which case I’ll treat myself to a glass of wine or a cocktail. My mother used to own a restaurant, so I know the markup on sodas and my beloved sweet tea, and I consistently choose water instead. Unless I’m at Merritt’s, in which case, a glass bottle Cheerwine is calling my name! — Jess

We haven’t had cable for a few years after switching to an HD antenna (works for football and the Bachelor franchise) and Netflix. We recently cut Netflix as well, because you can only re-watch The Office so many times. We’ve replaced watching TV with porch date nights and reading before bed. — Dave

I stopped buying books on Amazon, and I wait for library books now. It’s an exercise in patience, especially for popular titles, but I’m saving money and learning my bookshelves. — Jess

Saving money in your relationships:

We have gotten creative with ideas on how to spend quality time together without dropping so much dough – things such as trying out a new recipe at home, sitting on the porch swing with a bottle of wine, or going out for a beer at a new brewery. These all cost around $10, which enables us to have more date nights since we aren’t dropping $50+ on a dinner out. — Elizabeth Burns, eCommerce gal and house flipper

My love language is gift giving, and I save a ton of money by shopping at the Dollar Tree for all my wrapping paper, tissue paper, and extra giftable goodies like candy, small personal care items, cards, and balloons. — Samantha

Since having our son, we’ve realized how expensive getting a babysitter AND going out to eat is, so now, most of our “date nights” are on our porch with a bottle of wine. It gets us out of the house (if only to the outside of our house), and the only thing we’re buying is a $6 bottle of Trader Joe’s wine, rather than spending $25-30 on a bottle at a restaurant. But, my city-loving wife would be crushed if that’s all we did, so we also plan out special monthly date nights when we do hire a babysitter and actually head out. Scheduling them once a month gives us something really fun to look forward to, and keeps us from being tempted to go out on a whim and spend more than we had planned. — Dave

Since having June, we’ve been very open to borrowing, buying secondhand, or accepting hand-me-downs whenever possible. I think sometimes, especially if folks plan to have multiple kids, they justify buying everything new, but we’ve found it’s just as easy to swap back and forth with friends. We’ve borrowed clothes, a crib, a bathtub, a hiking pack, and so much more! – Em

Saving money on your home:

Target is my budget Kryptonite. I go in for toothpaste and come out with a new duvet, kitchen canisters, boots, and no toothpaste. One thing that has helped me save money is that instead of going into a Target for basics like toiletries, cleaning supplies, pet products, and some food items, I signed up for Target subscriptions. I can have all of these everyday items delivered to my house regularly (free delivery!) and subscription items are discounted by an additional 5%. This way I can still get my favorite Target items without having to actually go into a store and potentially blow my budget on all of the cute stuff I don’t need. — Elizabeth

When our grocery store offers 4x the fuel points on gift cards, we buy gift cards for upcoming projects/gifts – i.e. if we’re planning a home project, we get a gift card to Lowe’s in the amount we budgeted for the project. That way we earn 4x the points, and often get up to $1 off per gallon of gas! It takes some planning, but is well worth it in the end. — Valerie

Many products come in a generic brand version, a refurbished version, or a lightly-used version that’s practically the same for a fraction of the cost. You can often buy floor models for a highly discounted price, too, which we’ve been doing a lot recently as we furnish our new home. And remember, almost everything in life is negotiable – you’ll never know if you don’t at least ask! :) — Robyn Van Dyke, photographer, blogger, and co-owner of a dental practice (with her husband!)

We utilize the Habitat Restore. Since flipping houses is one of our side hustles, we visit the Restore often for anything from exterior doors, shutters, furniture, lighting, and faucets. A lot of big box stores will give donations so you can buy new items for a fraction of the cost while contributing to a good cause. There are also neat antique finds like gorgeous vintage chandeliers and clawfoot tubs. It’s definitely worth checking out if you are sprucing up your home on a budget! – Elizabeth

Saving money on purchases:

Starting around the midpoint of the year, I begin hoarding planned purchases like a fevered squirrel until I unleash them all on Black Friday/Cyber Monday. I keep a list of things I’d like to buy and that might go sale (so far this year’s includes Winter Water Factory dresses for June, her Salt Water Sandals for next year, and Walk in Love tees for the family for next Valentine’s Day). I also, of course, include as many Christmas gifts as I can! To make so many purchases in one weekend is always a bit of a shock to my system, but it’s totally worth it for the savings. – Em

ReceiptPal! My husband found this app where you take photos of your receipts and earn cash back for them, redeemable as gift cards (including Amazon!). We’ve earned over $100 in Amazon gift cards, which we then use for household purchases to save money. He spends roughly 10 minutes a week putting in receipts. It’s slow going — you usually only earn a gift card every four months or so — but totally worth it. — Valerie

Whenever we need or want to buy anything, we wait. This does two things: it gives us time to consider if we really need or want it, and it gives us time to find the best deal. Almost everything has a sale or coupon — it’s just a matter of waiting until the sale, googling for coupons, or even buying a coupon on Ebay! Better yet, wait for the sale AND stack the coupon AND use Ebates! — Robyn

We use a credit card with 2% cash back for almost every purchase, and pay it off twice a month, every single month. I know this might be controversial to some, but for us it’s a no-brainer. We’ve earned hundreds of dollars over the years this way! – Em

Saving money on everything else:

This has been a hard lesson to come by this year, but we’ve learned there are no “sacred cows” in our budget. To accomplish our savings goals, we’ve had to take a hard look at every single budget line and readjust our perspective (and add a heaping dose of contentment and gratitude). We might not be traveling to an international destination every third year like we had hoped, for example, but we still get to spend a week with our beloved families on the beautiful Connecticut shoreline. – Em

We worked to get the “big three” — house, car, and education — right. If you choose to buy these three things below (or well below, or not at all) your means and be content, you’ll have so much more financial margin and freedom. Our first home was tiny and it was subsidized by a non-profit for $115K, and then we recently purchased our current fixer-upper home after lots of negotiation for $200K. Our first car was $5K, and we were a one-car family for a couple years until we bought two new Toyotas for a killer deal by negotiating in cash and utilizing the TrueCar App. Education is a bit harder since much of it is outside our control, but we both chose to go to an in-state university and applied for as many scholarships and grants as we could. — Robyn

I get my hair cut twice a year, and I just get it cut – no dyeing, no fancy treatments. I LOVE my stylist, but she is quite expensive, so I compromise by extending my cut as much as I can. – Em

We keep our recurring bills low and cut where possible. We’ve never had a car payment and we’ve also never had cable. We also have never had an individual phone plan, because it’s so much more cost effective to add lines to an existing plan with a sibling, parent, cousin, or friend. You all save, so it’s a win-win! — Robyn

One big way we save money is by make a monthly budget and using cash only for things like groceries, gas, and household items. It is totally worth the extra time, intentional conversation, and planning – I’d say it has improved our marriage as much as our savings! — Samantha

We intentionally fill our evenings and weekends with everyday adventures so that we’re not tempted to mindlessly browse – either in a brick and mortar or online. I only go to a mall with a specific mission, and being outdoors and together helps keep us grateful, content, and in awe of the world around us. – Em

Friends, please join the conversation: I would LOVE to hear your favorite ways to save money! And thanks to all of the folks above for sharing their wisdom! :)

Affiliate links are used in this post!