Marvelous Money: Managing Money Together

As I wrote the How We Do It series, there were many topics – big and small – that I knew I would want to revisit at some point in posts of their own. When I got a few questions about how we jointly manage our finances in this post, I knew it was a great one to start with!

Using this beautiful image from Cultivate What Matters of the new Finance Goal Guide, launching today! If you have money goals you’re working toward, I think you’ll love this product!!

Many of the questions centered around why John and I have separate checking accounts. The short answer is that there’s no good reason – ha! Here’s the longer answer:

John and I have separate checking and savings accounts because we opened them before we were married, and there didn’t seem to be any good reason to open a new joint one after saying “I do.” After all, our accounts are at the same bank (and linked, so that we can access each other’s through our own dashboards!), and we of course have each other’s passwords. All accounts opened since our wedding day have been joint ones.

I know many people have strong opinions on joint versus separate accounts. I think many of the opinions, though, stop short of what’s truly important: the state of your heads and hearts trumps the practicalities of how your accounts are set up any day. All of the joint accounts in the world can still lead you to a dead end if you’re not pulling in the same direction.

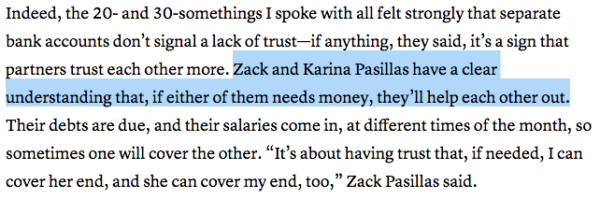

There is no “his money” and “her money” in our marriage. We have never valued each other or set individual spending levels based on what either of us make at our jobs. The idea of spouses effectively living at different income levels within a marriage is shocking and sad to me, as described in this recent Atlantic article:

They’ll help each other out?? Marriage means joining your financial future just as surely as it means joining your lives. I supported both of us while John searched for a job, and he put money toward my student loans for years without a peep of complaint. Were one of us to lose our job, we would not receive a “handout” from the other person – we would both adjust and bear the burden together.

On a practical note, the main reason there is no “his” or “her” money is that ALL money is fed into our family budget. At that point, we simply have one lump sum of money that we need to decide what to do with, together – it literally no longer matters who brought in how much. Because we’ve set the budget together, if it says we have a certain amount to spend, then that’s how much we have to spend. A budget is a great equalizer in this way, and if you need yet another reason to get on the budget bandwagon, there you go! :)

But back to the Atlantic article:

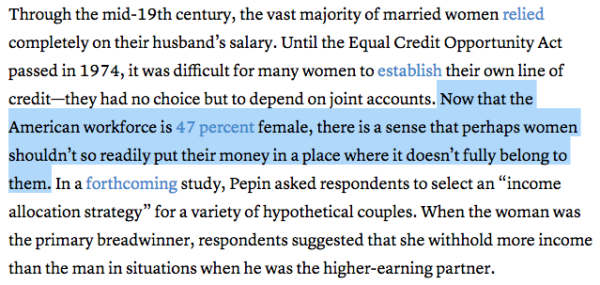

To that I would say, I don’t believe the money I bring home does or should “fully belong to me” — it’s shared with my husband, just as his money is shared with me.

Unsurprisingly, the arguments in the Atlantic article for why a couple wouldn’t merge their finances aren’t that compelling to me. There is one argument that I think does have validity, at least at the outset, but I don’t think it’s a situation that’s tenable longterm for a healthy marriage. If the two of you don’t have aligned beliefs on money, and aren’t consulting each other on where you’re hoping to go in life, then merging your finances absolutely will be a mess and will lead to arguments. The solution, though, is not to keep things separate — it’s to do the work to get on the same page.

John and I have a bit of an advantage here because we formed our thoughts on money alongside each other, but we also work actively to make sure we stay on the same page. (Hence our regular conversations and bimonthly net worth meetings!). Our friends Nancy and Will found themselves in the opposite situation: they came into marriage with VERY different ideas about how money should be managed. Financial Peace University helped them reach common ground, and they are some of the most inspiring financial stewards we know!

A final note, should you need more convincing: a joint budget not only determines your day to day spending on groceries, clothing, lawn care, and more, but it sets and guides your financial big picture, like how much you’re saving for retirement, how soon you’ll be able to get out of debt, when you’ll squirrel away the amount for a down payment goal, or how much you can give away each year.

And those big picture things? You want to work on them together, because then you will succeed together (and a lot more quickly than if you were working on your own!). There are few things more unifying in a marriage than reaching a major goal together, and if you’re not merging your finances, you’ll miss out on them.

Whew! Clearly this is a topic I’m passionate about, and that Atlantic article brought it all bubbling to the surface! To finish up, I’d love to hear: what goal are you working toward in your finances right now?

I LOVE this post and your arguments/philosophies here! I, too, am a huge advocate for wholly combining finances with one’s spouse for a plethora of compelling reasons (most of which you’ve laid out here). Even when Rob and I were dating (especially once we knew we were totally in it for the long haul), we began to think about it as OUR money. There is absolutely no division or keeping score when it comes to our finances, and it helps we both have very, very similar views on finances, money, short-term and long-term goals for our little family, and more. We’ve become really passionate about this topic and love working towards our goals together!

And right now, we’re in the (very frustrating) process of buying our first house! We’ve been diligently saving since day one of our marriage (especially once wedding expenses were finished with) and are so excited about how much we’ve been able to save over the last year. Now it’s just about finding the right house… and not being outbid every time!

Ahh, I don’t envy you searching for a home in Raleigh!! Such a hard market right now! But how wonderful that you have the money set aside when you do find the perfect opportunity! :)

I love your money posts! I think there’s a lack of conversation about HOW because we’re afraid it will become a conversation about HOW MUCH. I am so willing to talk about how my husband and I manage things and to me there’s no harm in that! Our budgets and structure have evolved over time and I find it so helpful to learn how other couples structure their finances.

Right now we’re doing everything we can to pay down debt and prioritize saving for some travel in the next couple years!

I love that, Ellie! I completely agree. A discussion of “how” is always appropriate to me, and so important! I learn so many things from watching how our friends “do marriage,” and I would love it if it was more common to pick up healthy financial practices from each other, too!

What an interesting read, my friend. Finances always seems to be a touchy one, especially in marriage.

Our situation is a little different as I don’t work – we have separate accounts (as opened before marriage) but they are linked together through banking for both of us to have access. I handle all finances in our home through both accounts but my husband is the only one who earns – so he essentially pays me a “Salary” each month.

I am currently saving for my trip to see you all in the Fall :)

x

I think combining finances is probably most important when one spouse doesn’t work, even as it’s also basically unavoidable! The possibility of hurt feelings on either side is elevated, I think, so it’s even more important to be unified on how you handle your money!

Whew! That Atlantic article is a doozy! :) I think the underlying logical flaw is that the author seems to misdefine a joint checking account as the husband’s checking account. She never acknowledges that a joint account is truly “joint” in that both parties have the password, equal access to the information, and equal abilities to contribute, monitor, and “control” the account! I’m not sure where she made the leap that a joint account means the wife won’t know what’s going on or be able to access the funds, but I wonder what she would say about a couple with a joint account where the wife does most of the maintenance? In any event, had she defined a joint account accurately, most of the arguments fall apart almost immediately. On a more important note, it seems the couple she’s describing place a higher value on their individuality than their sacrificial equal partnership, which is their prerogative, but in our house we have a different value system.

As I was thinking about this whole thing and the logistical inconvenience of having separate accounts, it occurred to me that about 95% of our expenses are indeed joint and shared expenses! Obviously our mortgage, groceries, vacations, household supplies, etc. But actually, even our student loans can be seen as joint since the financial benefit of that education is flowing to both of us! We do each have our own tiny budget for the 5%, which is mostly for clothes. :)

Right now we’re focusing on paying down student loans ASAP!

Completely agree on the central flaw! I almost included another pull quote where they talked about control of accounts because I found it so strange…

I don’t think they mis-defined it at all. It was literally within our lifetimes (I’m 32) that women would open credit card accounts and take loans without the permission of her husband. I was diversified on 2014, and dispite having joint accounts for the duration of our marriage and me being the ‘saver’ of the two of us, the judge ruled that because my husband made more money he was entitled to a greater share of our assets. No one wants to think of their marriage ending, but I would have been in MUCH better financial shape if we had kept separate accounts. The history of women having access to “family” finances doesn’t look good for women.

Hi Anon! I’m so sorry to hear that! I guess I’m a bit confused — if you had separate accounts, wouldn’t you have had a smaller share of money at the time of divorce anyway, if your husband made more money? This post was really more about money in a healthy marriage than preparing for every contingency. Personally, I am not going to make decisions about my life simply because the possibility exists that I might get divorced one day — I would much rather make smart choices based on the evidence I have that lead to the best possible outcomes I can see (in this case, choosing actions that I think help cultivate my marriage rather than protecting against a worst-case scenario). I know we are coming from different perspectives, and I appreciate you chiming in!

Love this! My husband and I, like you, had separate accounts coming into marriage and have kept them. We also have a joint account that our main paychecks go into to keep paying bills easier. I guess it’s kind of a hybrid of the two ideas, but it really works for us. We can surprise each other with gifts, treat each other to dates, or just spend fun money without having to think twice. Our joint account keeps our very unequal paychecks relatively equalized since it provides us one number to use for our budget. We pretty much never argue over money, and we both take active roles in trying to manage the finances. It’s fascinating to read how other couples manage money, thanks for the platform to openly discuss!

My husband and i do the same(ish)! We switched banks when we got married, so it looks a little bit different. We have a joint account where our paychecks are deposited, and where our big goal savings accounts are linked. But we also both have separate checking and savings accounts, which we opened when we opened the joint account, where we deposit our monthly “allowance” of walking around money for expenses we enjoy without the other person and for gifts. Basically, I don’t need to know what he spends on golf, and he doesn’t need to know about my shoes. I also love being able to take him on a date, or being surprised with a nice bottle of wine or a gift from him. I think it helps us not to feel stretched as we’ve saved for our house and paid back my law school loans.

Thanks you, Emily, for fostering this discussion, and writing such insightful posts. I love reading about personal finance, and especially from a woman’s perspective. I have learned so much from this series!

Love that solution, Kate! And so happy to provide the platform – I wish more people talked about this topic! :)

We’re working toward buying another car (maybe a van?!?! Do we take the plunge?) and refinishing our basement. All things we’ve talked about for a while, but with baby #2 on the way, it’s changing the timeline a bit. We shall see what we can save and what comes together!

This was so helpful to read in advance of my husband (we were married 5 weeks ago!) and I’s first big budget date this morning! We spent a LOT of time on Em for Marvelous, and are utilizing your budget spreadsheet! Thank you so much for all of the resources you provide on here, Em. It was beyond helpful for us, and made today a lot less nerve-racking than we anticipated! We are so relieved, and feel such a sense of freedom now that we have everything laid out and a plan for our money. Here’s to no longer wondering where it all went at the end of the month!

Bailey, this comment warmed my heart!! I’m so, so glad to read this. Here’s to many more money meetings to come! :)