Marvelous Money: Investing 101

Friends, I have wanted to (and promised to) write this post for years. While intimidation has kept it on the back burner (investing can be a complicated topic, and I wanted to get it right!), the desire to help and knowing I have something to share has kept it on the stove at all :)

Why? There have been a million articles written on investing, but sometimes you just need to hear it from a “normal person” – someone you trust. I hope I can be that person. Investing doesn’t have to be as intimidating and scary as it can sometimes seem!

So, here we are! My goal with this post is to begin to demystify the topic of investing for the beginner, to tell you a little bit about the difference it’s made in our life, and to give you the push you need to take the next step in your own investing adventure – whatever that might be!

Now is as good a time as any to issue my periodic reminder: I am not a financial planner, and nothing I say here should be construed as financial advice. I’m a gal who loves personal finance, has spent lots of time thinking about it, and wants to pass on what she knows!

Let’s start at the beginning, shall we?

What does investing even mean? Generally, you can understand investing as any tactic or vehicle to grow your money. It usually means assuming some amount of risk. You can invest in things like a CD (low risk), bonds (moderate risk), or an individual stock (high risk). And you can invest through vehicles like 401ks, IRAs, or brokerage accounts.

You can also invest in things like real estate, though for the purposes of this post, we’ll be sticking to financial assets (basically, money).

Why do people invest? Why might you want to invest? Investing allows you to harness the power of compound interest, which is putting your money to work for you – yes!! And when you reinvest your earnings, the pool of money you’re earning interest on grows, which begins a virtuous cycle.

Personally, investing my money is one tool in my financial independence toolkit. The more money I have (to a point), the more freedom I have throughout my life – to make decisions about how I live and give. This is motivating to me. And as a Christian, I believe it’s a part of stewarding what I’ve been given well.

Finally, on a very practical level, most of us need to save for our retirement. A common benchmark is that you should have 10x your ending salary saved if you retire at 67 (you’ll likely need more if you retire earlier). This is nearly impossible to do with the rate on a savings account (you’d have to save SO MUCH!), which is where investing helps you turn time into money (a.k.a. makes your money work for you).

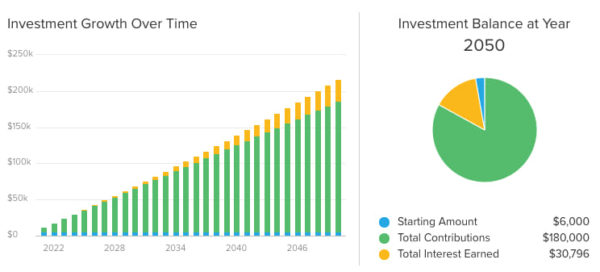

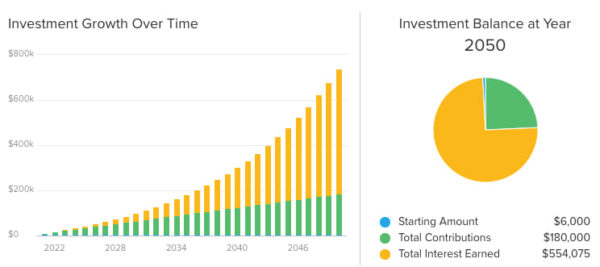

The graphs below illustrate this clearly: the top one shows a growth rate of 1% over 30 years, and the bottom shows a growth rate of 8% over 30 years. The ending balance is wildly different ($216k vs. $740k), and all of that difference is due to interest earned. Both go up, but you’re doing almost all the work in the first scenario.

Do I have to know a lot about investing to be successful? Good news – the answer is no! HOORAH! And it’s a good thing, too, because most of us don’t have the will, the skill, or the time to be investing experts. If you’ve attempted it, you’ve probably realized it can take a LOT of time and brainpower to research and manage your own investing portfolio. (My hand is very much raised here! There are dozens of things I’d rather spend my time doing than researching investments and investment strategy!)

So, how to be successful? Here’s the key: you have to embrace the fact that you’re a novice, and make choices to safeguard against your weaknesses. You’re looking for something that will construct your portfolio for you, and manage it on an ongoing basis. Here are three options:

Option 1: A target date fund. If you have a 401k through your work, you’ve probably encountered this investment vehicle before. They’re an extremely common offering in plans because they’re simple and they prevent big mistakes, ha!

A target date fund is an entire diversified portfolio (US stocks, international stocks, bonds, etc.) in one package. It knows when you’ll need to start using the money (your target date, or prospective retirement date) and automatically rebalances to become less risky in its investment mix as you approach that date. For example, it might start out with a 90/10 mix of stocks (higher risk) and bonds (lower risk) when you’re 25, and shift to a 50/50 mix in your 60’s. And you won’t have to take any action to make that happen!

If you choose a target date fund, that’s hypothetically the only thing you’d need to invest in! Experts consider them most appropriate for retirement accounts if your retirement is still pretty far away (20+ years?), because they are simple and not individualized to your unique needs. (After all, they only know one thing about you: when you want to retire. They know nothing, for example, about your comfort level with risk.)

This is what I used in my old 401k!

Option 2: A robo advisor. Welcome to the future! :) This is a digital investment service – just a computer algorithm, with no person behind the scenes – that constructs and manages your portfolio for you. To determine your investments, it will ask you a few questions about your situation, preferences, and goals, then split your money across investments. It will automatically rebalance your investments periodically, and may check in with you periodically, too, to see if your situation has changed.

The pros: it is more tailored to you than a target date fund, and it’s low cost since there’s no person involved. The cons: there’s no person involved :) There’s no advisor who’s taken a deep dive into your situation to help you develop a plan to meet your financial goals.

Though most people use a robo advisor in addition to their 401k for retirement savings, we experimented with using one for our mortgage payoff account. (We liked it, but are currently trying something else!) Most large investment firms, like Fidelity and Schwab, and small firms, like Betterment, have robo options to explore. Here’s a place to start!

Option 3: Wealth management. This option (the most personalized) gets you a trusty sidekick for every part of the investing journey! Your advisor will consult with you on the full breadth of your financial life (your goals, tax situation, upcoming life events, desires, preferences, etc.), and then they’ll use that to design and manage a tailored financial plan and investment strategy.

Unsurprisingly, this is the most expensive option because of its comprehensiveness and customization, and there will likely be a minimum amount of money outside of your 401k you need to have available to invest. (This amount varies, but is probably around $250k+, depending on the firm/advisor.) Often, the higher your balance, the lower the fee, so the higher your balance, the more appealing (and useful!) of an option it is.

If you’re ready to go this route, you might start by looking for an advisor wherever your 401k is housed, or ask for recommendations from trusted friends. And look for someone who is certified as a CFP, or Certified Financial Planner, the gold standard in this industry.

WOW THAT WAS A LOT! Just a few more things, friends.

What can I do to set myself up for success as an investor? A few final suggestions:

1. Honestly evaluate whether you have the will, the skill, and the time to manage your own investments. Remember that one of the biggest dangers to your investment success is you!

2. Remember that investing can feel stressful in the short term. Choose a wise strategy that accommodates your weaknesses and strengths and then check in only at designated intervals.

3. Invest consistently, even when the market goes down. That’s when you’ll get the best deals :)

What is the best way to get started with investing?

1. Start now! Start small, if needed! Remember the power of compound interest.

2. If you have a company match in your 401k, start by contributing enough to meet the match.

3. If you’re already meeting the match, consider increasing your contribution.

4. If you don’t have a 401k, consider opening an IRA. If you already contribute to an IRA, consider increasing your contribution.

5. If your retirement goals are on track, consider opening an investment account, an HSA, or a 529 plan and contributing toward another big goal.

Friends, I’d never be able to answer all of your individual questions about investing, but I hope this post has served to demystify the topic a bit. Accessing the power of the stock market has been incredibly impactful even in just our first decade or so of “adult life,” and I know that power will only grow as compound interest continues to work its magic – and I hope the same for you!! I’m most definitely cheering you on as you take your best next step, and would be happy to answer any follow-up questions below! :)

I’ve eagerly been waiting for this post and am so glad you wrote it! I got very lucky, and my boyfriend has a long time (15+years) relationship with an advisor, and we have a meeting set for tomorrow to set up my account after a detailed discussion on goals. Without your original posts from many years ago I would never have considered this, but am so excited to begin my journey and watch it grow over the years!

That makes me so happy, Kelly! And what a gift to get to work with someone so trusted!

Love this post! Thanks for sharing. Investing has always felt very intimidating to me. After a couple years of learning, I was able to read your post and understand just about all of it! haha. After my husband and I got married, we started meeting with a financial advisor to help us get started on the right track with managing our finances long term (401K, IRA, HSA, paying off student loans, etc). It’s been so helpful to have someone trustworthy make the process a little less intimidating while helping us gain further financial literacy.

So good, Jaime!! It’s taken me years to get to this place, too :) And still so much to learn!

This was a great intro! My husband and I work with a wealth management advisor, and he’s been incredibly helpful for us. For example, it was such a relief to have someone look through all of the different funds available for my 401k (I had a lot of options – far more than is typical) and hand pick the right allocation for me/my goals. I think sometimes people are reluctant to invest in the cost of working with an advisor, but it really paid off for us (puns fully intended, ha!).

I think that’s so true, Megan! So many of us don’t hesitate to spend money on other professional services, but balk when it comes to financial advice… which doesn’t really make sense when you think about the outsize effect working with an expert can have on the money we have to spend in the first place!

This is such a well-timed post; we’d been considering whether/how to invest our tax return! I wonder if you’d consider a future blog post on ethical investing options and/or what control the average investor has over where their money goes (for example, I personally would not want to invest in fossil fuels). After reading this blog for years, I expect that’s a topic you’ve also thought about! :)

Thank you for writing this post!

Thank you SO much for this; it is exactly what I needed! I feel so validated that other commenters had the same thoughts, and now I don’t feel so intimidated about this concept!