Marvelous Money: Paying Off Our Mortgage Early

In my last Marvelous Money post, I shared our current Big Goal: paying off our mortgage early, in the next five years. I’ve had some questions about how and why we are doing that, so I thought we could chat about it today!

Why we are paying off our mortgage early:

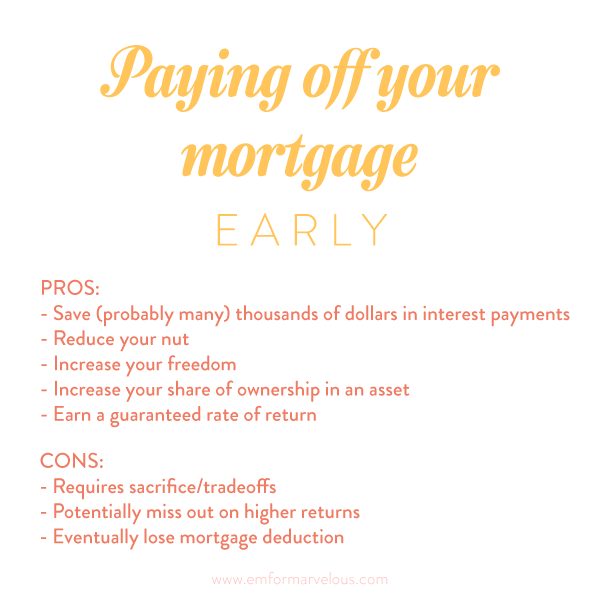

Though paying off our mortgage early seems like a slam-dunk choice to us, there are pros and cons. Here are a few:

To expand a bit on these reasons:

— Save (probably many) thousands of dollars in interest payments: By paying off our mortgage more than 20 years early, John and I will save roughly $120,000 (!!!!!) That is a LOT of vacations and dance lessons and flights to see loved ones and delicious dinners out over a lifetime. That excites us!

— Reduce your nut: Megan McArdle describes your financial “nut” as “the amount of money that you absolutely have to pay every month if you don’t want scary-looking men to start repossessing your possessions.” Think: fixed expenses like car loans, student loans, mortgages, and the electric bill.

— Increase your freedom: The smaller your nut – the fewer obligations you have per month – the more freedom you have. If your nut is tiny, you can quit your job for one you love with a lower salary, or start your own business, or stay home with your kids. You can travel, or support charities that matter to you, or buy the most delicious-looking food at Whole Foods every week.

— Increase your share of ownership in an asset: As you pay off your mortgage, you’re buying more and more of your house from the bank and building equity (money in your pocket if you choose to sell one day!).

— Earn a guaranteed rate of return: You can think of eliminating a future payment as earning a guaranteed rate of return. For example, if your mortgage has a 4% interest rate, you’re effectively earning 4% interest on the money you use to pay off your loan.

On the other hand…

— It requires sacrifice and tradeoffs: This is the hard part, as we already discussed! For us, paying off our mortgage early means forgoing vacations, reducing our grocery budget, delaying clothing purchases, cooking at home, (almost) never going to the movies, not purchasing alcohol, and more.

— You potentially miss out on higher returns: The most common argument against paying off your mortgage early is that if you instead invested those extra payments in the stock market, you could earn a higher rate of return (since the stock market averages 9ish% per year over the long term). While this is true, it’s also true that most people don’t have the willpower to actually set aside that money and watch it build without dipping into it.

— You’ll eventually lose the mortgage deduction when you pay off your mortgage: This is true, but it’s still not a good reason to keep your mortgage, because the math doesn’t work out. Dave Ramsey explains more here, but the upshot is you’d always be paying more in interest than you’d save in taxes.

For us, the freedom and peace of mind we will gain from having no mortgage before June enters school far outweighs the sacrifices we’re making now and the potentially higher returns we’re missing out on.

Photo by Anna Routh – see more of our home here.

So that’s our why! Let’s talk about our how.

Very simply, we’re paying a set amount per month over and above our normal payment. Since we live and die by our budget, we’ve found that budgeting for that expense just like everything else has been the most helpful instead of waiting for “extra” funds to pop up.

When we first started attacking our mortgage three years ago (after we paid off our student loans and car loans), we did the simplest thing: we put the extra money directly toward our mortgage. (Our mortgage lender allowed us to make manual online payments, which we did every month.)

A year and a half ago, however, we decided to take things up one more notch by aiming for the best of both worlds. Since the main critique of paying off a mortgage early is that it doesn’t make sense to pay off a low interest rate mortgage when you could be earning higher rates of return by investing, we decided to invest the extra money we had been paying toward our mortgage.

So, instead of directly applying the money to our mortgage, we now transfer our extra payment (the same amount as before) to a brokerage account every month, where it is invested in a mutual fund. When we reach the full amount we need to pay off our mortgage, we’ll pay it in one lump sum. That will be a sad day for our bank account, but a happy day for our assets :)

A word of caution: I would only consider doing our “next level” system if you have a long track record of steely willpower with your money. It is so tempting to just take a little here or there as we watch that fund grow and other needs come up, but for this plan to work, you have to consider it absolutely untouchable!

Also, this approach requires a willingness to take the risk that the money you’re saving for paying off your mortgage could actually lose value.

If you’re nervous you’d be tempted or don’t want to stomach the risk, just apply the extra payments straight to your mortgage – done and done. Also a fantastic option.

Our master bedroom – photo by Callie Davis

We’ve still got a few years to go, but once we get under $100k owed, I think we’ll make a visual countdown somewhere in our home! I remember watching the Rays $90k chalkboard countdown dwindle month after month whenever we went over for dinner. SO exciting, and such a great teaching opportunity for kids!

One caveat and one piece of encouragement before I sign off of this exceedingly lost post.

Caveat: Paying off your mortgage early may not be the right money goal for you right now. Dave Ramsey considers it baby step 6 of 7, after paying off all other debt, building an emergency fund, and saving for retirement and college. It is an awesome goal, but one you should probably tackle after everything else is squared away.

Encouragement: Just because most Americans have a mortgage doesn’t mean you have to!! When you live like no one else, you get to live like no one else – free from worry about money, and at peace with whatever the future holds. If paying off your mortgage is important to you, I truly believe you can do it! I’ll be cheering you on!!

There’s about a million more things I could add to this post, but I’ll leave it there for now! If you’d like to read more about paying down debt in general (including info about how we freed up enough money in our budget to make our extra payments), click here.

I’d love to hear: Are you hoping to pay off your mortgage early? What financial goal are you working on right now? What’s holding you back from getting ahead with your finances, or where do you feel you need the most help?

As always, I loved reading your perspective on this. We’ve gone so back and forth and ultimately for us the better fit was investing the lump sum we had saved into a rental property, which now pays for both mortgages each month. There is a certain amount of risk involved, however, but we’ve already seen the property value increase so we’re hopeful that it will pay off for us long term. I love what y’all are doing though.. and can’t wait to follow your progress! I’ve been hyper aware of our spending lately, I think just because we’ve reached a point of starting to add really noticeable amounts to our grocery bills since having Beau. Time to call a budget committee meeting, haha! Grateful that you share on money, a topic that can be kind of awkward to discuss but that ultimately is like any other area we need to be diligent in caring for!

Awesome! Yes, risk isn’t inherently bad, you just have to know how much you’re comfortable with! I hope a rental property is in our future, too! :) Always thankful for your encouragement, friend!!

Dillon and I have been talking about this a lot lately – the timing of your post couldn’t be better! It’s on my heart to do this someday, as it opens up so much opportunity for generosity and adventure. Thank you for sharing your heart on this topic Emily! :)

Currently (emphasis on currently) the interest on a mortgage, even a fixed one is cheap debt. Using funds otherwise spent in paying off a mortgage (or more if one owns more than one home) stocks or other investments *currently* (again, emphasis on currently) is a far better deal for those that are savvy, and depending on your level of knowledge in this area, this yields much (in some cases, enormous yields) more coming in than going out. Also, factor in the tax benefit of the amount of mortgage being held. That being said there are taxes on those enormous yields…however, like vehicle speed and gas usage, there is a sweet spot.

If you are not savvy in this department being mortgage free is definitely the best road. Dave Ramsey is a great educator for those looking to get a grasp on their financial lives.

The financial control you have displayed is excellent and is to be commended. Financial freedom equals freedom, period. If more people realized this the world would be a happier place. But, it is not our job to make others happy – it is their responsibility. Figuring out this joy is a developmental phase in the human psyche – it can not be spoon fed.

It should be noted that one is never debt free in this realm, as property and state taxes will be with you and your heirs until death. Great job!

Hi Susan! So happy to have your perspective! I agree, it’s hard to forgo higher returns, which is why we’ve decided to invest our extra payments instead of applying them directly to our mortgage. Hoping to get the best of both worlds! :)

While you are absolutely right that property and state taxes will always be an expense, I would consider them a fixed payment, not a debt, since you’re not paying interest on them.

You are such an inspiration! As always, I love this Marvelous Money post. Thank you, Emily! I dream of the day that my husband and I pay off our mortgage. We purchased a one bedroom “starter” condo in DC a couple of years ago, which we’re planning to rent out when we grow out of it. In the meantime, we’ve rid ourselves of all other debt (my credit card mistakes before marriage, my student loans, and his car payment), have fully funded an emergency fund, we’re on track with retirement and future college savings, and are now working on aggressively saving for a “new” (used) car (to pay in cash ;), saving for a baby, and our next down payment! I think our biggest challenge is knowing how to prioritize our savings goals, in a way that’s realistic for our timeline.

Sounds like you’re doing an amazing job, Megan!! I definitely empathize with your challenge, but the good part is, you’re already doing the most important thing, which is saving – decisions beyond that are kind of just like icing on the cake! :)

Bookmarking this to revisit later when I’m ready to buy a home! Honestly, the home buying process gives me anxiety! Do you have any other blog posts about it? :)

I wrote a few blog posts about the search for our house, but have been wanting to write a separate post about financial things to consider when you’re ready to buy. Hopefully I’ll get to that sometime this year!

You know I love this!! I couldn’t agree more about “the freedom and peace of mind” outweighing the sacrifices and potentially higher returns you’re missing out on. Cheering you on and can’t wait to celebrate with you when you make it happen! :)

Love it, especially since this was LITERALLY our lesson last night. Cheering for you!! Xoxo

Yes!! Love this! We’re in this process as well. We decided two years ago to get serious and pay off our house. We are counting down the months and hope to finish this year. Woohoo! As a very analytical numbers gal (it’s what I do!) I took a little longer to come around to this being the right option for us since our interest rate is so low. However, we looked at what the Bible has to say about debt and that changed my mind. We also are looking forward to the day when we have zero payments- huge amount of freedom and possibility there that’s truly priceless. Keep us updated on your progress- it’s motivating to read about other families who are working in the same direction!

So fabulous, Lindy!! I definitely will :)

I love that you are so open about this! I wanted to create a visual countdown in our kitchen, but I was self conscious about it since we often have others over in different stages of finances over including those much older than us. It can be so motivating to have friends who openly talk about financial discipline, however, we live in Northern Virginia where middle class homes are often 500,000 and few people have them paid off. Maybe I shouldn’t have been embarrassed, but I was embarrassed that we had the means to pay ours off at 29 when many of our friends were still working on grad school loans. Since we paid our home off this fall we have been enjoying a few months of more extravagant planned purchases Ex. We are putting in a Pickett fence, a small deck, and we installed a gas fireplace in our sunroom. While these are expensive items hopefully they will increase our home value. We are now buckling down and saving up for a new home in a better school district, but we aren’t planning on Moving for 3-4 years. In the meantime we’ll enjoy our paid off home, new deck, and continue to invest in a mutual fund for the next home. Paying off our house allows me to work part time and spend the extra time with my 1 year old. I’m so thankful we took Dave Ramsey a few years ago and I just wish we had done it when we were engaged. Best of luck paying off your home- I know you two will do it! What are you looking forward to the most about the financial freedom it will bring?

Gillian! I think we should be friends! :) With the Rays countdown, they didn’t have a huge banner over it that said “debt-free countdown” or anything like that, they just had the numbers listed out on their chalkboard. I liked that it was clear to family members and anyone who asked, but also not braggy or in-your-face!

LOVE, love, love what you shared about life post-mortgage. At this point, I am most looking forward to being able to travel more, potentially working fewer hours, and not having to worry so much about the cost of traveling to visit our families!

Gillian! I just have to chime in and say how helpful that visual countdown was for us! We started with 7.5, 7, 6.5, 6, 5.5…. all the way down to 0. We knew it represented the $75,000 balance we had left on our mortgage, but not many other people knew that other than friends or family. But when people asked, we joyfully told them! We found it was more inspiring than it was “in your face…” even though we were certainly nervous about doing it at first. It was a great conversation starter. I hope you consider the countdown! (And you can see actual photos of our countdown in this post if you are curious! http://nancyrayphotography.com/financial-freedom-•-part-4/ )

Thank you for your wisdom in this difficult area! We have been completely overhauling our budget and rethinking our saving/investing strategy recently. I really appreciate your willingness to share the strategies you’ve taken time to learn and implement. I often get overwhelmed by all the things we should be paying off and saving for and investing in, but this conversation made me think about the way that stewardship is really about self-discipline, patience, and trust in the Lord, one goal at a time.

Yes. The really good news is that though there might be some definite “right” order of saving, as long as you’re working toward SOME goal, it’s hard to go wrong! Cheering you on!

I really enjoy your money posts! You and I live completely different lifestyles, but I similarly follow/love having a set budget. I’m glad you explained why you want to pay off your mortgage early. I still have no desire to pay off my mortgage early LOL Maybe one day I will? Not to get all “soap boxy” but having chronic health problems gives me a different perspective. First I think, where do I get the extra money to pay off my mortgage early when I have to pay a 20 percent coinsurance on any medical procedure/doctor’s visit + prescription medicine? “Sick families” already have more of their paychecks drained compared to a healthier family because being chronically ill is costly.

And second, the idea of putting my extra money after medical expenses toward my mortgage doesn’t fit in with my overall life philosophy, so I’m sure that’s why I could never commit to it. But the one thing that comes through in your money posts–one reason I enjoy them– is that you can meet any money goal you set if you are fully behind your reasons for doing it.

Love your perspective, Jewel. I will freely admit that our financial progress is aided by excellent health insurance and generally healthy family members! And I completely agree with you – the only way you’ll achieve a financial goal without being miserable in the process is if the goal perfectly aligns with your values and goals!

Loved this post and enjoyed reading all of the commentary! I let my husband who has an MBA in Finance handle all our financial stuff, so I usually don’t have much of an opinion on our money. I just feel so blessed to be able to swipe my debit card at Dunkin Donuts each morning and not ever worry about money in the bank! :) I know that is such a blessing and that we are so fortunate.

We are big Dave Ramsey fans too, but I agree with comment #2 about the mortgage interest being cheap debt (yet…still debt, I realize). I think our 30 year fixed was 3.2%. For us, since we already put very large percentages into our 401K, tithe, save for our son’s college, etc, it makes more sense for us to invest in the stock market and other residential/commercial properties, which we currently do.

I’m not sure I could sacrifice my frequent splurges (Chick-fil-a and Dunkin) to pay off our loan sooner. But then again, when I see that post on Em for Marvelous when you are debt free in your thirties, I’ll be like “Darn…I should’ve sacrificed that Spicy Chicken Sandwich!” ;)

I’m loving the different perspectives, too! And yes, definitely not the right goal for everyone right now! Rest assured, I still eat my fair share of no. 1 CFA meals with a chocolate chip cookie – one of my favorite splurges :)

Emily-I am so so encouraged by this post. My husband and I have been debating putting our extra payments into a brokerage account at the recommendation of an advisor but I’d never heard of anyone doing that. I’m glad to know we wouldn’t be the only ones!

Oh i love this. So aligned with you girls this week. I painted my nails last night (Jess’s post) and I worked on my vision board last night and DEBT FREE- particularly mortgage free is my main goal. I feel like I can’t let myself “dream” of “things” because this goal has my heart. Watching my parents go through bankruptcy several years ago and watch them rebuild theirselves has inspired me and rooted me in this goal. I believe God calls us to be free and debt is so enslaving. I cannot wait to extravagantly give. The past two years we have made it a discipline/worship to tithe and it has truly made me even more passionate about stewarding well.

Yes short term sacrifices can be hard but I think that’s why vision boards and goals are so important! Saying no to things becomes exciting because you know it is serving a bigger purpose. Love your money posts! And also loved Nancy Ray’s journey too!

Well you KNOW I am doing a major happy dance over here!!!!! HUZZAHH!! We will be majorly celebrating with you when you pay that final payment!!

Love the idea about sticking your savings in a mutual fund until you have the balance to pay off the mortgage. I had never thought about this way to get the return, while still saving to pay off the mortgage. Makes so much sense, especially if your mortgage rate is on the low end which most recent mortgages are. Will definitely be adopting this in the Kirk household! Thanks Thomases!

Always proud when I can teach Dave Kirk something new :)

[…] large enough to, say, make a huge difference in our mortgage (and we already feel good about our progress and plan there), but it was enough to make our backyard project a reality. We were SO excited to start the […]